Integrity’s new pricing, what does it mean for you and your clients?

Integrity’s new pricing, what does it mean for you and your clients?

What are the changes?

Integrity Life takes an industry stand, by removing unnecessary and archaic fees to make it more affordable for everyday Australians to get protected. We have also sharpened our pricing in the following areas:

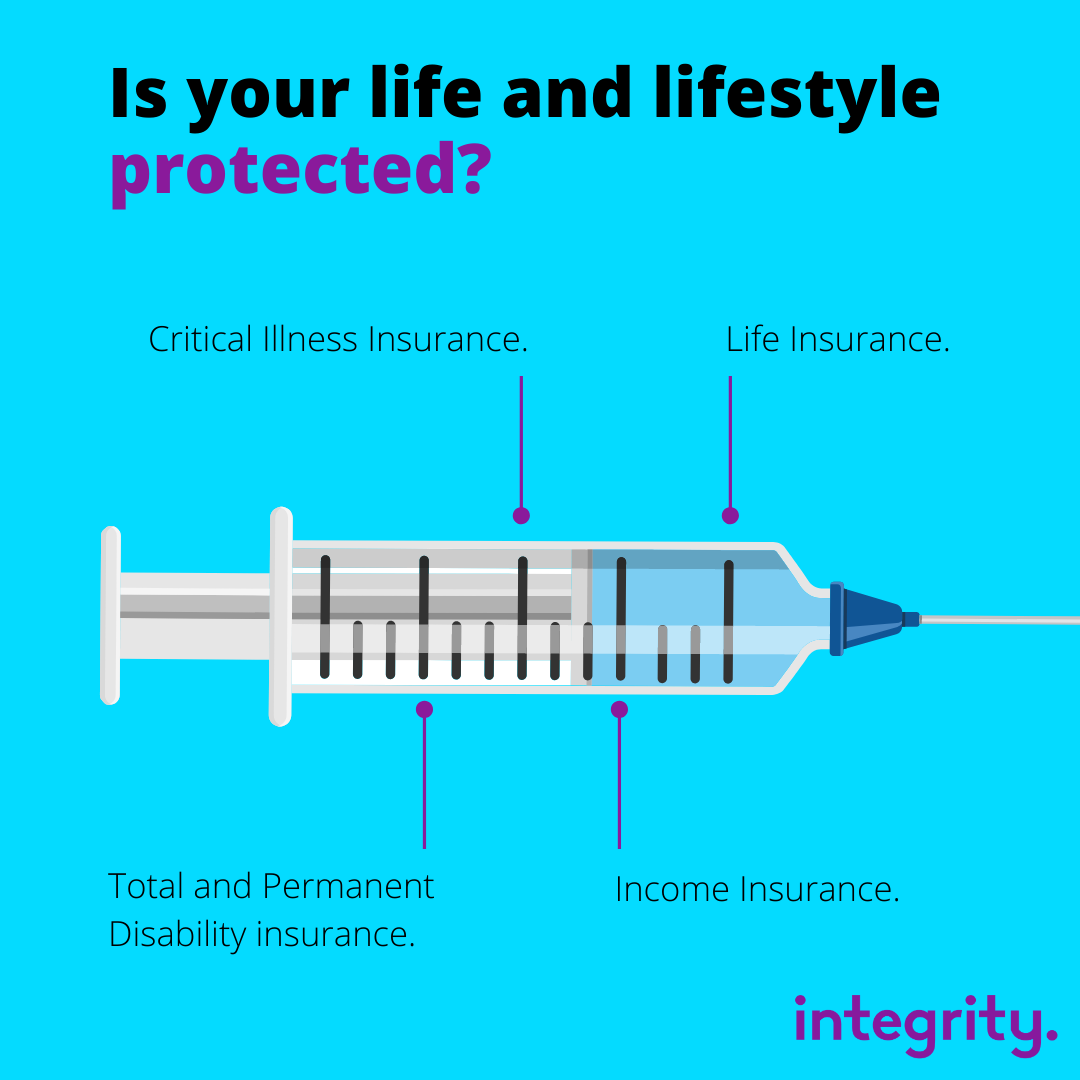

- Packages of Lump Sum covers with and without Income Insurance

- Clients aged 30-50

- White and light blue occupations primarily

- 2- and 5-year Income Insurance Benefit Periods

Not every possible client scenario will result in a decrease in premium especially standalone Age 65 Income Insurance. However, our combination of premium reshaping, removal of monthly premium loadings along with our approach to not charging policy fees, 2-year base premium rate guarantee, and laser like focus on efficiency, we believe we’re making the cost to serve clients more attractive for Advisers, which will allow more people to benefit from the value of Financial Advice and the protection of life insurance.

What about monthly premium loadings?

Integrity has also removed unnecessary, additional fees to pay monthly insurance premiums for all new business, another outdated legacy which hasn’t kept pace with changing consumer expectations and experiences. Our GM of Sales, Marketing, CX and Product outlines why Integrity has taken a stand on this important issue. “We believe that clients should be able to pay by the month at no extra cost. The long-standing industry practice of charging additional loadings when premiums are paid monthly just doesn’t stack up anymore. It imposes an unnecessary cost on policyholders at a time when affordability is such a critically important consideration for most everyday Australians. We believe it’s time that we move on from such archaic industry practices and open our industry up to more customers who need the peace of mind of being adequately protected.”

Why has Integrity made these changes?

Our MD and CEO, Sean McCormack said it best “This represents a significant shift in our focus as an insurer towards providing protection for more everyday Australians. As a digital first insurer we have both the capability and modern customer experience that is aligned with what these everyday Australians expect and need in our changing and evolving world. Life insurance can’t remain analog in the digital age, and this is a further step to help provide protection for more Australians. This combined with our laser like focus on operational efficiency for our partners, means we have a compelling proposition to take to mainstream Australia and deliver meaningful benefits to them by being insured with a modern, contemporary insurer.”

I have more questions, what should I do?

Please reach out to your Integrity Life BDM, but if you’re new to Integrity then please contact us here and we would be happy to assist you.

Please note.

This information has been prepared without considering your personal objectives, financial situation or needs. Before acting on it, please consider its appropriateness to your circumstances.

Integrity Life

From the newsroom