It’s time to cut through the noise on Income Insurance.

It’s time to cut through the noise on Income Insurance.

To say there has been a lot of ‘noise’ across the industry since the launch of the new IDII products in October 2021 would be an understatement. With the conversations focused heavily on product features and definitions and how they compare against previous iterations. While important especially when considering existing clients and their circumstances, the more critical conversation is about how advisers will adjust their ‘house view’ on Income Insurance as a result of these changes and have the changes gone far enough to ensure the future of Income Insurance as a sustainable product option.

The sustained financial losses experienced across the industry have been widely document and speak for themselves. APRA is a prudential regulator not a product regulator, however they were compelled to step in and take action as a result of their assessment about the overall strength and sustainability of the industry from an Income Insurance perspective. APRA’s intervention was unprecedented and far reaching. No one in the life insurance ecosystem (clients, advisers and insurers) have been immune from the impact associated with the poor experience seen across the industry over the past number of years. No single insurer was going to be able to facilitate the necessary change, hence the reason for APRA’s intervention.

APRA’s intervention was based on one key principle – sustainability. It’s important to note this isn’t just a product and pricing change – it’s a holistic change including philosophy, approach & strategy, operational practices, risk and governance, along with data management. There has been a lot of debate in the market about why and how we got to this point, and while this is interesting the reality is that if these changes didn’t occur, it’s unlikely we would have Income Insurance products in the future.

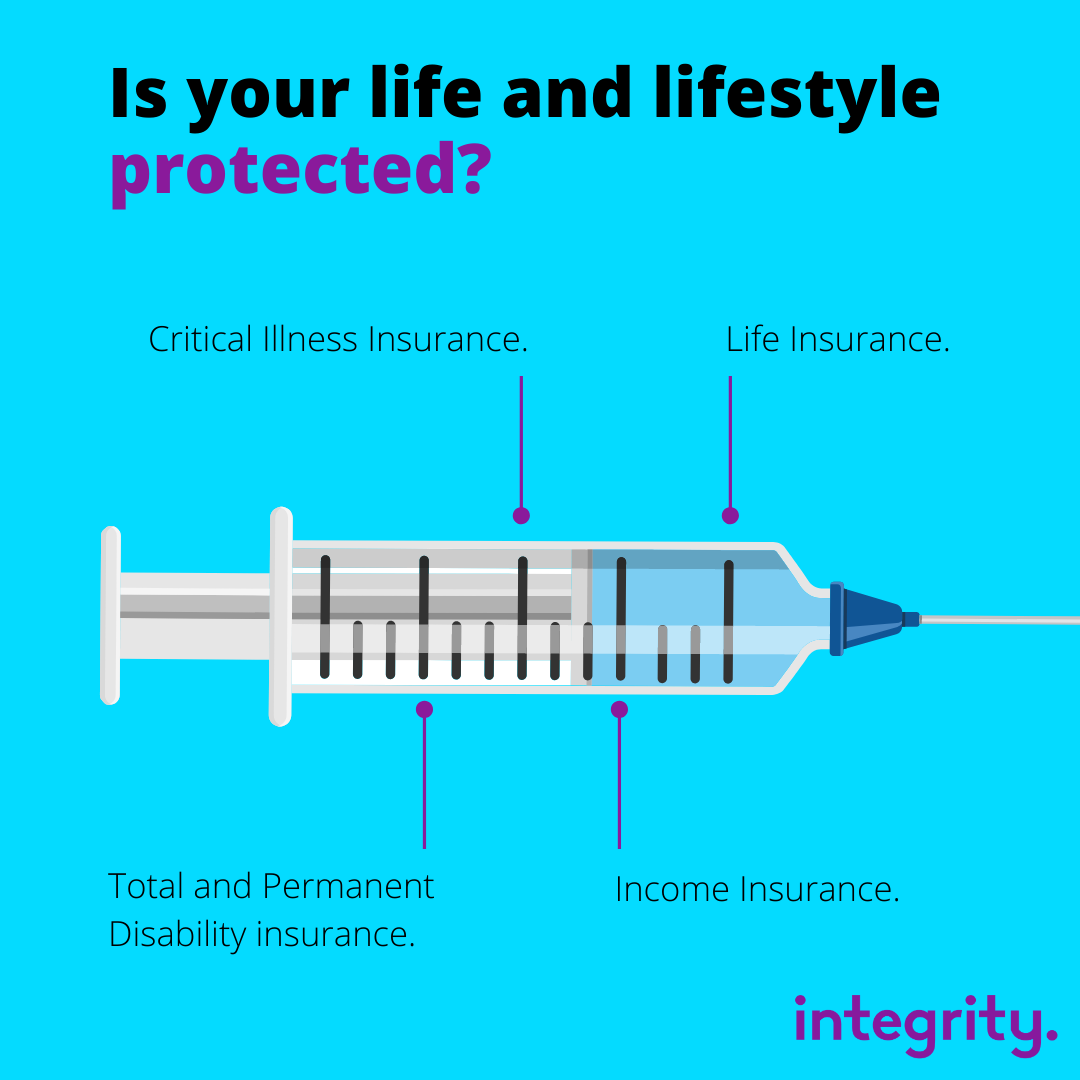

APRA’s expectations combined with the Actuaries Institute’s IDII Reference Product and Sustainability Guide laid out some clearly defined “guardrails” for insurers in respect to product design and pricing that were about re-setting the product back to its fundamental purpose. Providing financial support by replacing part of a client’s regular income if they are unable to work due to accident, illness or injury.

Interpretation of these ‘guardrails’ has been mixed and varied across insurers but ultimately APRA will be considering whether the industry has delivered on what it was asked to do and assess accordingly in early 2022.

The days of the industry seeing most applications being submitted on maximum Monthly Benefit amounts, 30 Day Waiting Periods, to Age 65 Benefit Periods at the cheapest price may well be changing. IDII products in the market now are all quite different and determining which product is most appropriate becomes more subjective than ever. Therefore, considering how Income Insurance will be used in the advice process is something that needs a conscious rethink by advisers moving forward. Matching shorter term Income Insurance benefit periods such as 2 & 5 years with complementary lump sum covers is expected to be part of the considerations that advisers will make as a result of the changing landscape.

As an industry, we all have a collective responsibility to ensure Income Insurance products exist to support people when they need it most. However, we need to step up our game and not go back to the ‘old ways’ and more traditional mindsets. What was done in the past won’t work in the future. The longer the benefit period, the greater the uncertainty and the higher the risk of future premium increases.

Now is the time for advisers to contemplate what these changes mean for their insurance ‘house view’ moving forward and challenge the conventional thinking about Income Insurance as the world as we knew it has now changed forever. While this may be our collective reality, the one thing that remains consistent is the need for and the value of professional insurance advice.

Russell Hannah

General Manager Sales, Marketing & CX.